Commentaires de gestion

6 mars 2025

European Credit: Unlocking Value Despite Spread Compression (en anglais uniquement)

The spread compression that has defined credit markets throughout 2024 may lead some investors to hesitate when allocating capital to the asset class. However, RAM AI believes that European credit remains an attractive opportunity, supported by compelling fundamentals and market dynamics.

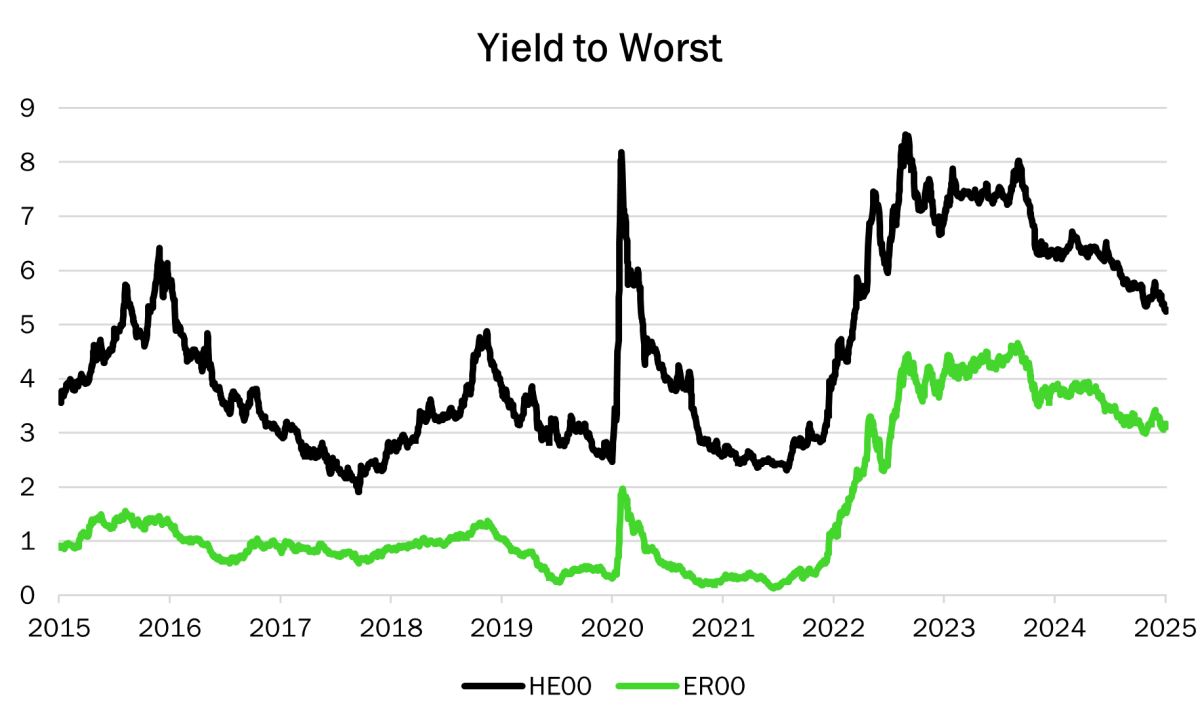

Yields remain high relative to the last decade

As of January 2025, absolute yields in European credit stood above the 80th percentile of the past decade.

Figure 1: HE00: ICE BofA Euro High Yield Index ER00: ICE BofA Euro Corporate Index. Source: Bloomberg, RAM AI, as of 21st February 2025.

With the European Central Bank’s easing cycle underway, cash rates are expected to decline in the coming months. However, we believe there is still a compelling opportunity to generate attractive income. Steep credit curves should help anchor the longer end of the market and create the potential for capital appreciation as bonds naturally shorten in maturity, with yields drifting lower as they ‘roll down the curve.’

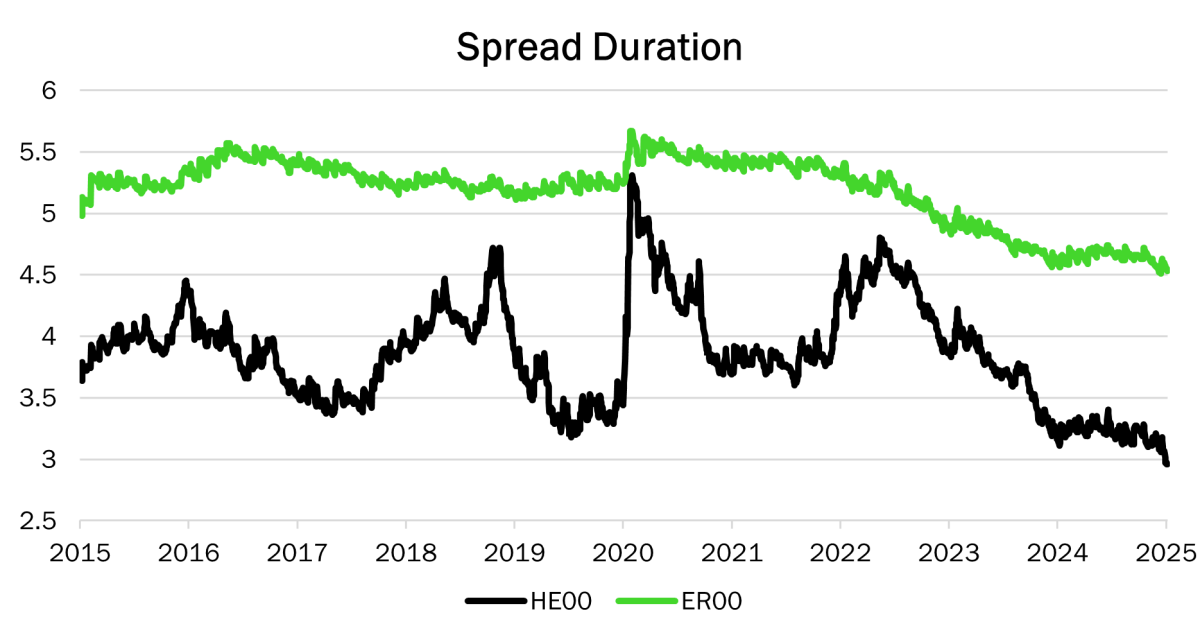

Spreads look attractive on a relative value basis: shorter-duration markets support tighter spreads

The duration of European credit indexes has been declining significantly. Sub-investment grade issuers have opted to retain older bonds issued before the recent cycle of rate increases, capitalising on their lower interest payments, while higher-rated firms have primarily issued bonds with shorter maturities due to their lower financing costs. Simultaneously, the depreciation of longer-dated bonds has reduced their overall weighting in the market. These dynamics have led to European corporate bond markets becoming much shorter in duration than they were at the close of 2021.

Figure 2: HE00: ICE BofA Euro High Yield Index ER00: ICE BofA Euro Corporate Index. Source: Bloomberg, RAM AI, as of 21st February 2025.

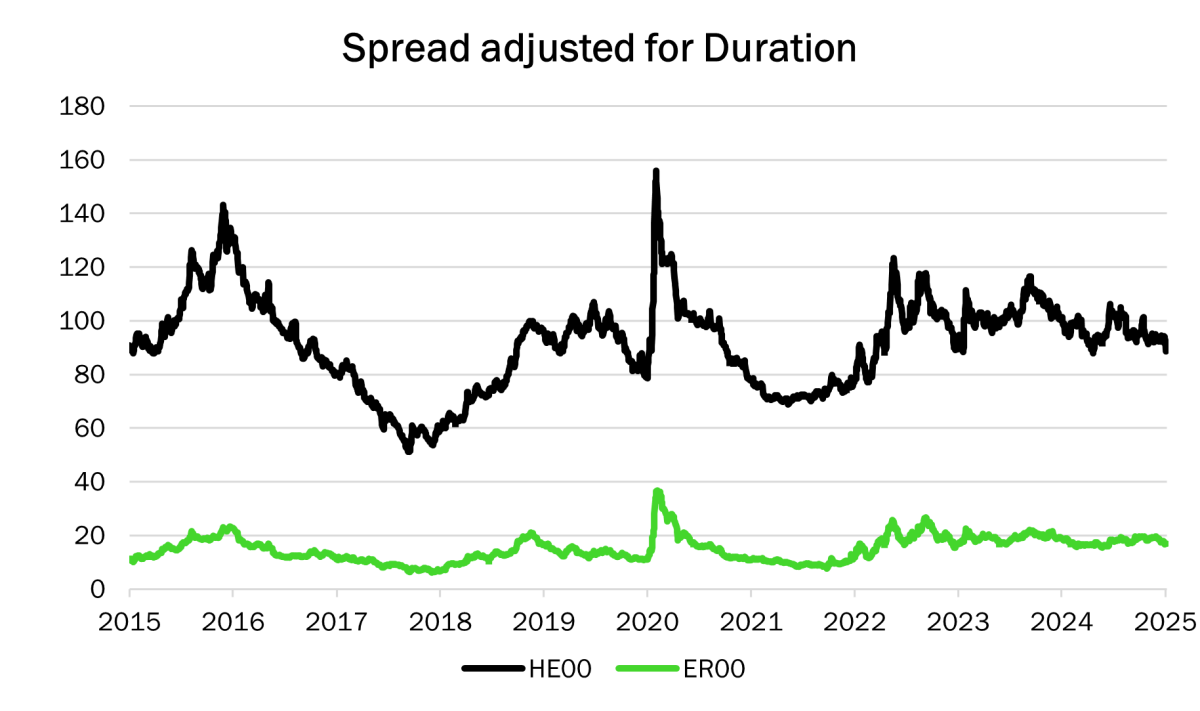

To accurately assess the value in the market, we adjusted spreads for their respective duration. The data indicates that, for each unit of duration, High Yield (HY) bonds currently offer nearly 100 basis points (bps) of spread, while Investment Grade (IG) bonds provide over 20bps. At the end of 2024, spreads in European credit markets were approximately 50% higher per unit of duration compared to their tightest levels in 2018 and 2021. By this metric, European credit spreads appear to have room for further tightening.

Figure 3: HE00: ICE BofA Euro High Yield Index ER00: ICE BofA Euro Corporate Index. Source: Bloomberg, RAM AI, as of 21st February 2025.

By adjusting for duration, we get a better sense of compensation per unit of risk. Investor concerns around spread valuations may be alleviated if we acknowledge that the risks that those spreads reflect are also lower than in the past.

Fundamentals remain solid across the universe

In aggregate, we believe the European credit market benefits from a resilient fundamental backdrop that should help navigate potential market uncertainties with greater stability and confidence.

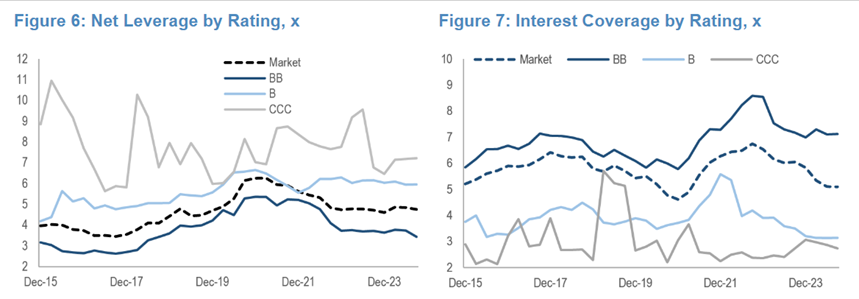

The aggregate interest coverage ratio, which measures a company's ability to cover the interest payments on its outstanding debt, of our credit universe is above the 80th percentile of a period of observation running since 2002 and normalising after a period of very low rates (2015-2021). Similarly, the median net leverage continued to move downward in 2024, trending back towards pre-COVID levels. Interestingly, earnings trends driving the metrics were roughly a 50-50 split on companies seeing EBITDA (Earnings before interest, taxes, depreciation and amortisation) growth vs contraction. Leverage trends by rating continues to flag the dispersion in outcomes between the higher and lower rating bands, with BBs tracking an average 3.6x, back at levels last seen in 2018 while CCCs remain high.

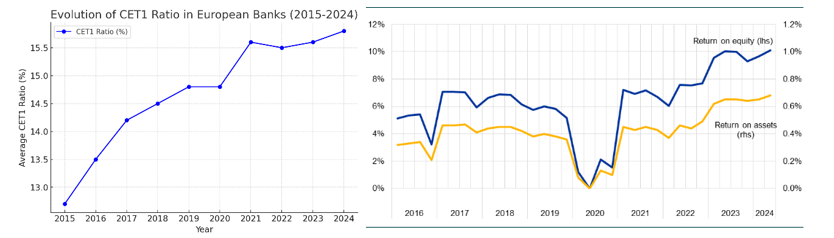

European banks are underpinned by solid fundamentals, supported by strong capital buffers, improved asset quality and resilient profitability. Regulatory reforms over the past decade have strengthened capital positions, with Common Equity Tier 1 (CET1) ratios well above regulatory requirements. Non-performing loan (NPL) ratios have declined significantly, reflecting better risk management and a healthier economic environment. Additionally, higher interest rates have boosted net interest margins, supporting earnings despite a challenging macroeconomic backdrop.

Net leverage and interest coverage are trending down in the European corporate world…

Figure 4: Source: JP Morgan, data as of end of December 2024.

….. while capitalisation and profitability for banks have never been higher

Figure 5: Source: EBA, data as of end of December 2024.

Conclusion

In a scenario where credit demand remains robust and economic or political risks stay under control, our assessment indicates that spreads have still some room for tightening, particularly in the current landscape of exceptionally elevated yields and strong fundamentals.

by Fabio Vanerio & Vincent Ollivier

Credit Management & Advisory Team

Legal Disclaimer

Ce document a été conçu à titre purement informatif. Il ne constitue ni une offre ni une sollicitation d’achat ou de vente des produits d’investissement qui s’y trouvent mentionnés et ne saurait être considéré comme un service de conseil en investissement. Il n’est pas destiné à être distribué, publié ou utilisé dans une juridiction où une telle distribution, publication ou utilisation serait interdite, et ne s’adresse pas à une personne ou entité à laquelle il serait illégal d’adresser un tel document. En particulier, les produits mentionnés ne sont pas offerts à la vente aux Etats-Unis ou dans les territoires et possessions de ce pays, ni à aucune personne américaine (citoyens ou résidents des Etats-Unis d’Amérique). Les opinions exprimées ne prennent pas en compte la situation, les objectifs ou les besoins spécifiques de chaque client. Il appartient à chaque client de se forger sa propre opinion à l’égard de tout titre ou instrument financier mentionné dans ce document. Avant d’effectuer une quelconque transaction, il est conseillé au client de vérifier si elle est adaptée à sa situation personnelle et d’analyser les risques spécifiques encourus, notamment sur le plan financier, juridique et fiscal, en recourant le cas échéant à des conseillers professionnels. Les informations et analyses contenues dans le présent document sont basées sur des sources considérées comme fiables. Toutefois, RAM AI Group ne garantit ni l’actualité, ni l’exactitude, ni l’exhaustivité desdites informations et analyses, et n’assume aucune responsabilité quant aux pertes ou dommages susceptibles de résulter de leur utilisation. Toutes les informations et appréciations sont susceptibles d’être modifiées sans préavis. Les investisseurs sont invités à fonder leurs décisions d’investissement sous la forme de souscriptions en parts aux rapports et aux prospectus les plus récents. Ils contiennent des informations supplémentaires sur les produits concernés. La valeur des parts et les revenus qui en proviennent peuvent s’apprécier ou se déprécier et ils ne sont garantis en aucun cas. Les produits financiers mentionnés dans ce document peuvent voir leur cours fluctuer et subir des baisses soudaines et importantes allant jusqu’à égaler la totalité des sommes investies. Sur demande, RAM AI Group se tient à la disposition des clients pour leur fournir des informations plus détaillées sur les risques associés à des placements spécifiques. Les variations de taux de change peuvent également provoquer des hausses ou des baisses de la valeur de l’investissement. Les performances antérieures, qu’elles soient réelles ou simulées, n’indiquent pas nécessairement les performances à venir. Le prospectus, le Document clé pour l’investisseur), les statuts et les rapports financiers sont disponibles gratuitement au siège social de la SICAV et de la société de gestion, auprès du représentant et distributeur en Suisse, RAM Active Investments S.A., Genève, et auprès du représentant des fonds dans le pays dans lequel les fonds sont enregistrés. Le présent document commerciale n’a pas été approuvé par aucune autorité financière, il est confidentiel et toute reproduction ou distribution totale ou partiale dudit document est interdite. Emis en Suisse par RAM Active Investments S.A. Société agréée et réglementée en Suisse par l’Autorité fédérale de surveillance des marchés financiers (FINMA). Emis dans l'Union européenne et l'EEE par la société de gestion agréée et réglementée, Mediobanca Management Company SA, 2 Boulevard de la Foire 1528 Luxembourg, Grand-Duché de Luxembourg. La source des informations susmentionnées (sauf indication contraire) est RAM Active Investments SA et la date de référence est la date du présent document, à la fin du mois précédent.