News

15 March 2022

2022: Has the time (finally) come to go market-neutral?

At a time of unprecedented uncertainty and rich Equity valuations, there are few investments that can contribute to decorrelate returns and reduce risk in portfolios in the case of larger Equity downsides, and we believe it will be the case for the Market-Neutral asset class.

The succession of the 2018-2019 Value Crash and the COVID crisis hurt the Equity market-neutral asset class significantly. The dispersion of valuations kept widening in favor of Growth stocks over the rest of the market, hammering short books.

The hit was only worsened by the massive flows out of the asset class, culminating in the “Big Short Tantrum” of 2021, with short covering leading to record low short interest in the US market.

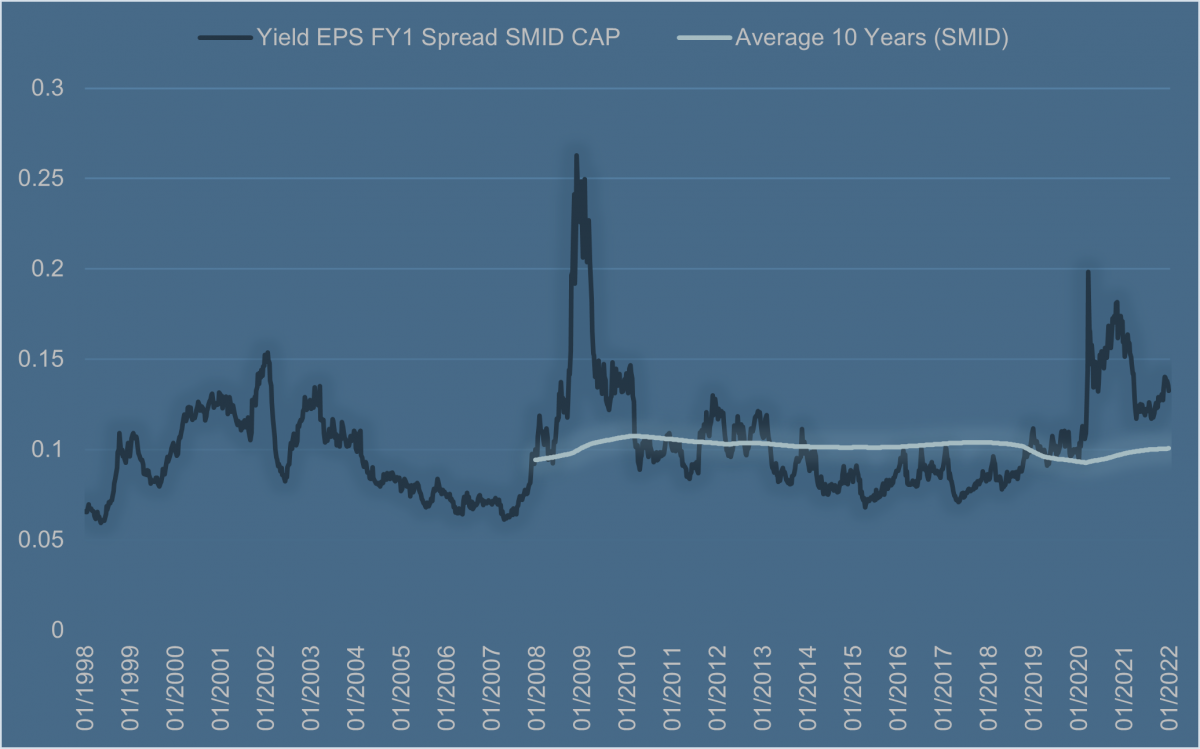

Some segments of the Growth universe had reached extremely high levels of valuation, pushing the dispersion in valuation further than during the Tech Bubble, and to the highest levels since the 2008 stock dislocation. The process of normalization in valuations that has started since end-2020 has been favorable to a recovery of fundamentals-driven stock selection approaches, at the expense of thematic Growth stocks.

We flagged the opportunity then, and we have since started to see dispersion tighten back, leading to the beginning of a strong recovery of fundamental-driven Market-Neutral strategies.

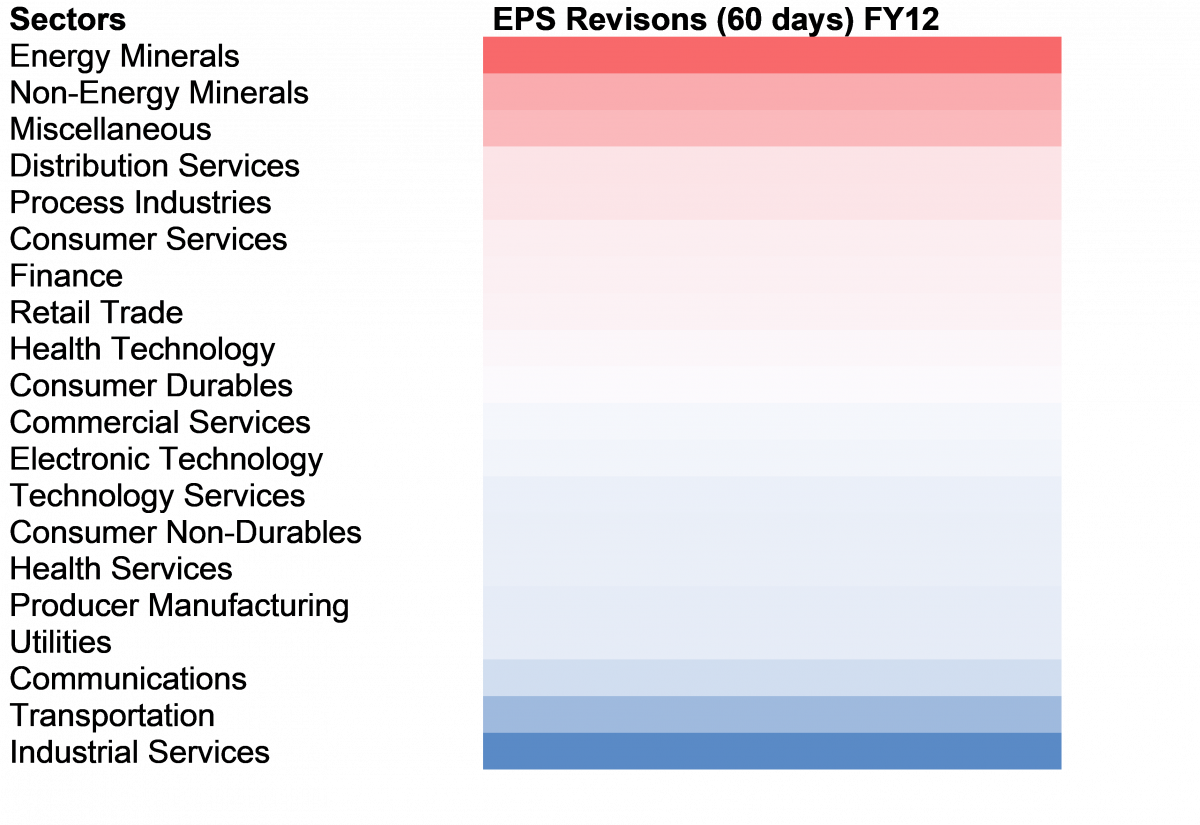

Dispersion of earnings yields across small and mid caps, within RAM Equity Universe

Source: RAM AI as of 31.12.2021

Real or simulated past performance is not a reliable indicator of future results.

Source: RAM Active Investments as of 28.02.2022, Please refer to note [A] at the end of the document.

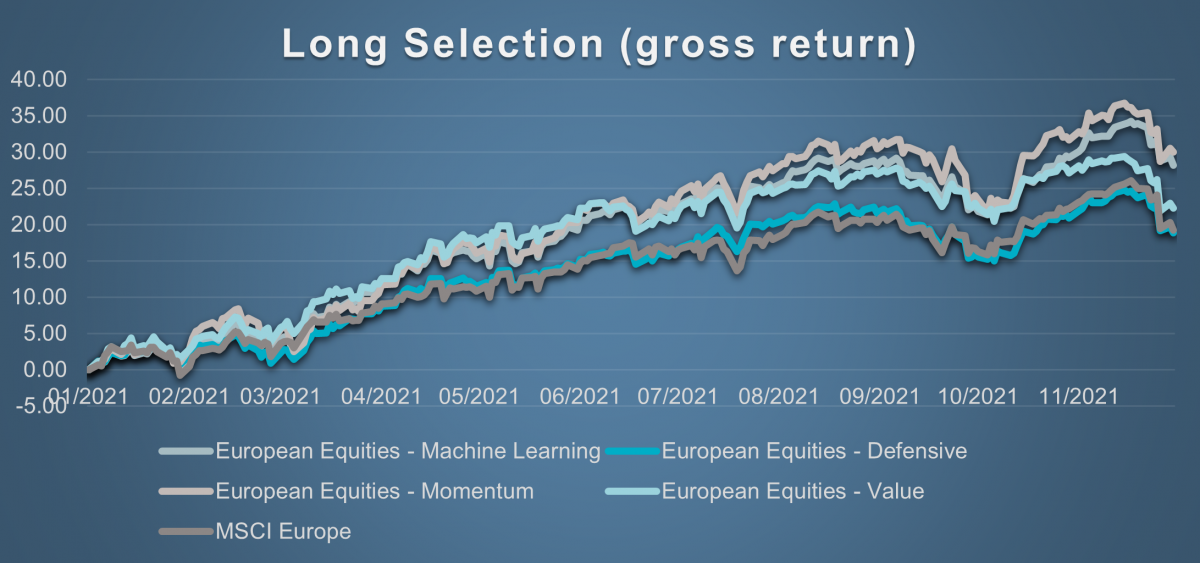

The highly expensive Growth stocks in the Biotech, Renewable Energy, Software,… industries that we picked on the short side of the book started converging back in our favor since March 2021, concurrent with the start of the demise or ARKK ETFs in the US, which epitomized the bubble in Thematic Growth Investing.

Source: RAM Active Investments as of 28.02.2022, Please refer to note [A] at the end of the document.

The still higher-than-average levels of dispersion in European and global markets, as well as the anticipated start of a tightening phase by central banks, should a priori be a further boost for relative-value strategies, as speculative growth stocks correct further on the back of more expensive financing costs and higher interest rates shortening the duration of investments.

In addition, we currently see large dispersion in earnings momentum across industries, creating more relative value opportunities across the market.

Source: RAM AI as of February 2022.

The dispersion in fundamental valuation across the market is reflected by an attractive asymmetry of valuation within our market-neutral strategies in Europe and globally.

|

European Market-Neutral Strategy |

|||

|

Long Book |

Short Book |

MSCI Europe index** |

|

|

BEst Dividend Yield |

3.4% |

2.5% |

3.4% |

|

BEst P/E |

13.0 |

25.2 |

13.7 |

|

FCF Yield |

7.9% |

0.0% |

6.2% |

|

ROE |

17.8% |

-5.1% |

14.3% |

Source: RAM AI, Factset Fundamentals.as of 28.02.2022

“*Benchmark selected for specific illustration purposes only in this marketing material. There is no benchmark in the official documents of the fund implementing the strategy”.

The valuation gaps are even more striking on a global basis, as Growth/Thematic trends have been even stronger in the US, with sometimes very stretched valuation gaps supported by retail flows in the last years, as evidenced by the horrendous fundamentals (highly negative free-cash flow yield/roe) of the names shorted in the book.

|

Global Market-Neutral Strategy |

|||

|

Long Book |

Short Book |

MSCI World index** |

|

|

BEst Dividend Yield |

2.6% |

1.4% |

2.1% |

|

BEst P/E |

14.1 |

50.4 |

17.3 |

|

FCF Yield |

7.5% |

-4.7% |

4.6% |

|

ROE |

31.7% |

-6.5% |

16.1% |

Source: RAM AI, Factset Fundamentals.as of 28.02.2022

“*Benchmark selected for specific illustration purposes only in this marketing material. There is no benchmark in the official documents of the fund implementing the strategy”.

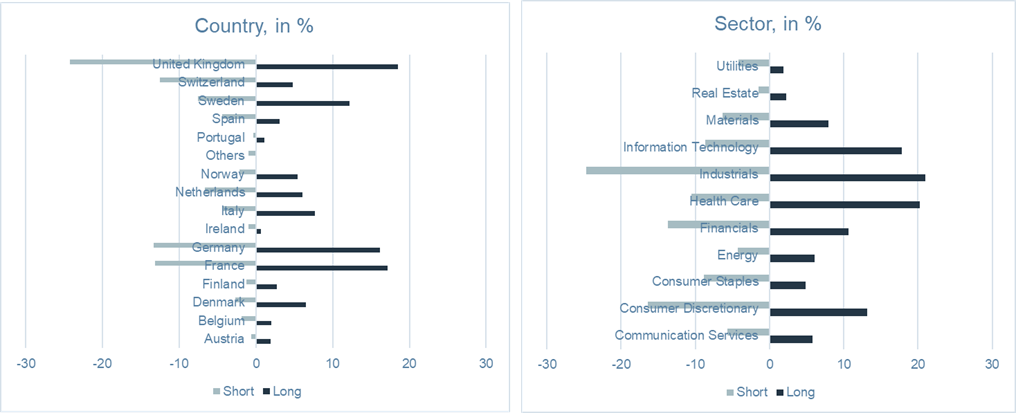

The latest trends in the RAM Long/Short European Equities portfolio are towards an increase of net IT, Health-Care and net Energy/Materials exposure, the fund capturing the current cyclical risk and the inflationary trends pressuring the economy.

Source: RAM AI as of 28.02.2022

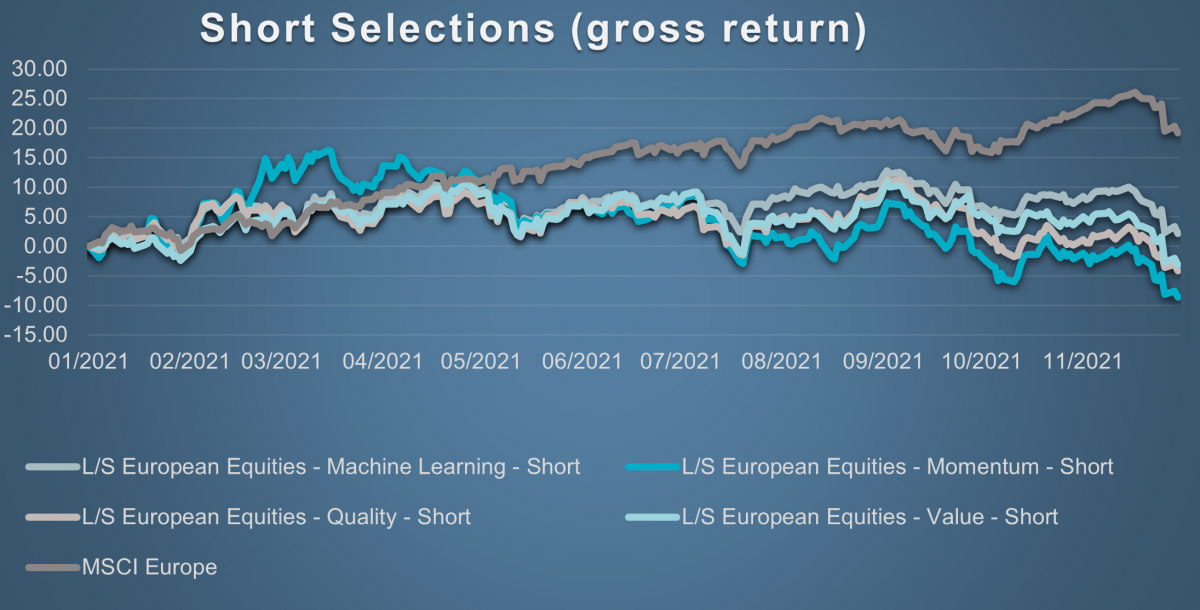

In terms of style, this is our ability to generate alpha across our selection engines that we believe will add value for our shareholders. As illustrated in the below charts, on the short Book, all our selections of shorts (Value, Momentum, Agnostic, Quality) underperformed the market, contributing to positive alpha generation for the fund.

Market Capitalisation

Overall, either in Europe or in Global Developed countries, our strategies identify opportunities across the market cap spectrum. We tend to identify even more Short pick opportunities in the Small Cap segment than Long opportunities (given the large number of companies with fragile fundamentals and excessive investment/financing needs), resulting into a net Short bias on Small Caps in the book, which tend to prove useful in large liquidations as in 2008.

Conclusion

High valuation, earnings and return dispersion should keep providing an interesting opportunity set for Market-Neutral strategies. The current geo-political risk only magnifies the risks for the global economy, already about to be fragilized by the exit of central banks’ easy money policy. Market-Neutral strategies which were hurt on their Shorts by easy liquidity should prove useful to investors when direction is reversed.

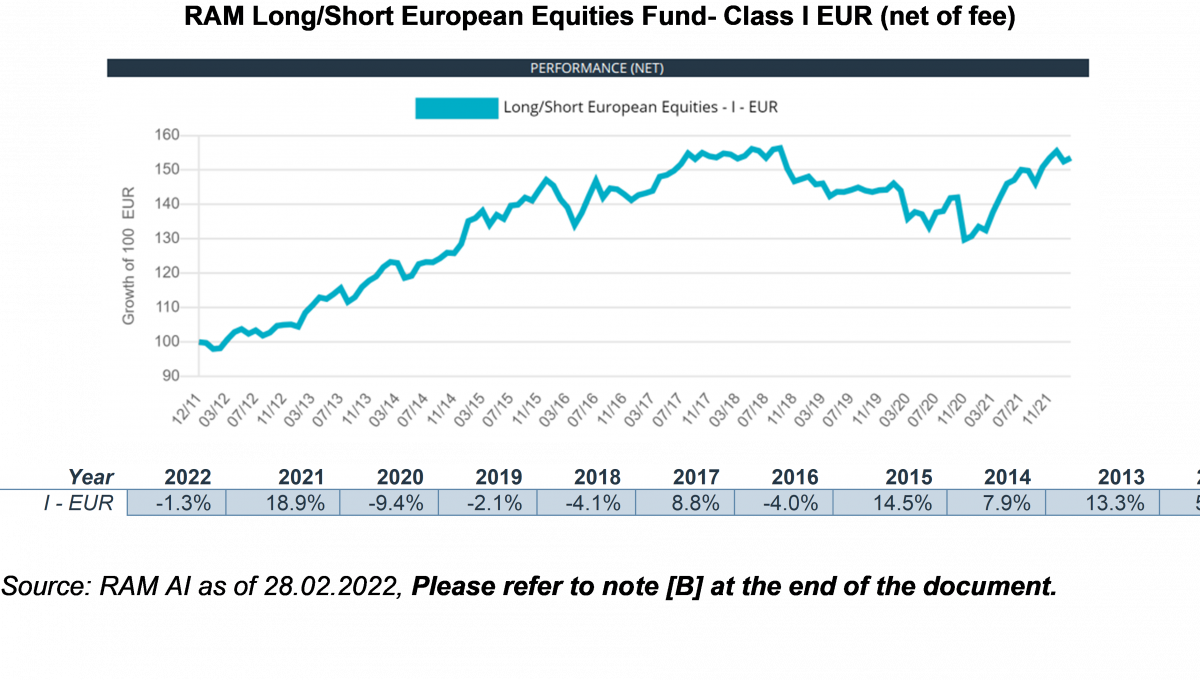

Realized Track Record

Real or simulated past performance is not a reliable indicator of future results.

Note [A]: The real portfolio strategy exists since 2011 and it does not include any reference to a benchmark. This graph shows a sub-strategy performance including a benchmark for pure illustrative purposes. Sub-strategy performances are calculated based on simulated model portfolios rebalanced monthly on RAM equity investment screenings and may not represent the exact contribution of strategies in real portfolio.

The sub-strategy cannot be invested. Sub-strategies performances are here adjusted considering their long-term theoretical fixed allocation in the strategy and to match the GAV performance therefore should serve for informative purposes only. The graph represents gross performance in euro

Note [B]: The performance data do not take into account fees and expenses charged on subscription and redemption of shares nor any taxes that may be levied. There is no guarantee to get back the full amount invested. Changes in exchange rates may cause the NAV per share in the investor's base currency to fluctuate. Please refer to the Key Investor Information Document and prospectus with special attention to the risk warnings before taking an investment decision.

The I EUR class is currently registered in Austria, France, Italy, Germany, Luxembourg, Netherlands, Switzerland, Spain, Sweden, Singapore (foreign restricted scheme) and United-Kingdom. The sub-fund may be registered in additional countries.

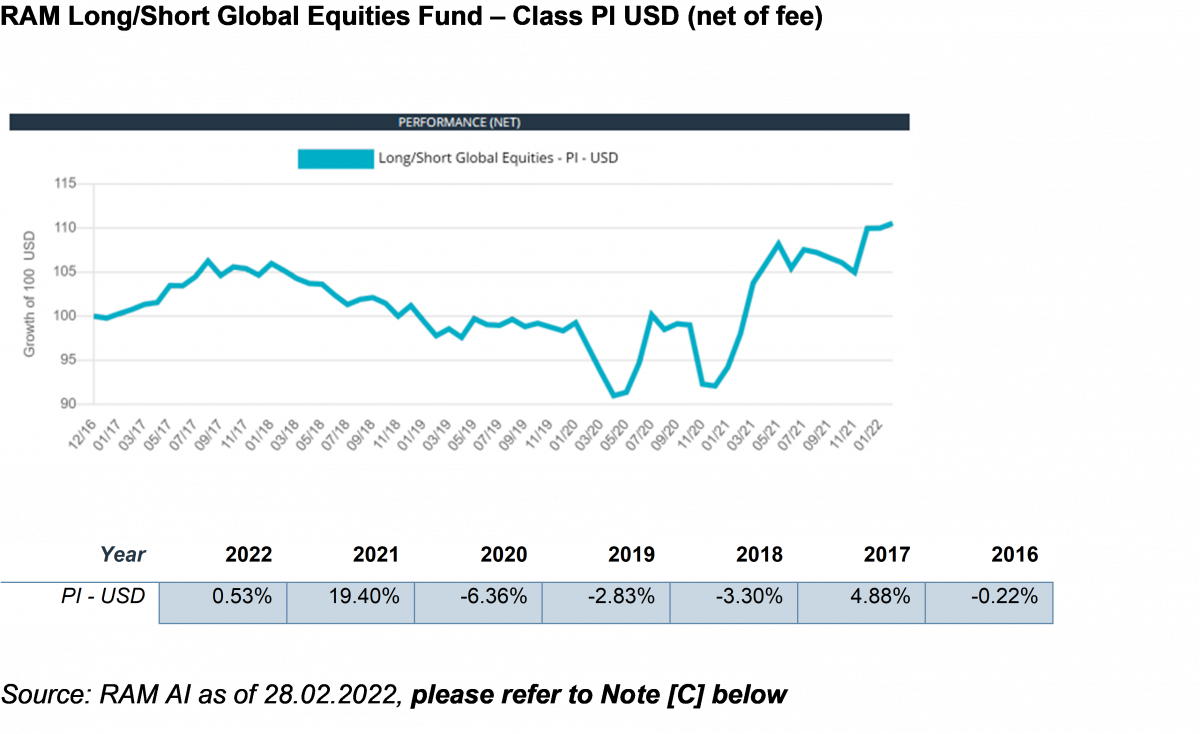

Note[C]:The performance data do not take into account fees and expenses charged on subscription and redemption of shares nor any taxes that may be levied. There is no guarantee to get back the full amount invested. Changes in exchange rates may cause the NAV per share in the investor's base currency to fluctuate. Please refer to the Key Investor Information Document and prospectus with special attention to the risk warnings before taking an investment decision.

The PI USD class is currently registered in Denmark, Germany, Italy, Norway, Switzerland, Sweden, Spain, Finland, Singapore (foreign restricted scheme), United-Kingdom. The sub-fund may be registered in additional countries.