Commentaries

7 November 2019

October 2019 - Risk concentration building up across portfolios - Systematic Fund Manager's Comments

The direct consequence of unconventional monetary policies across the globe, which are undeniably related to lower economic growth and inflation, is the formation of risk concentration in financial markets and ultimately into investors' portfolios. Risk concentration is ultimately a source of significant volatility. The main potential sources of volatility we see in this current environment are:

- Central Banks’ Policy

Central banks are navigating in unchartered territory; negative nominal rates are abnormal and the consequences for the economy are poorly understood. Additionally, an increasing number of voices are questioning the transmission mechanism of negative interest rates policy through to the real economy.

- Global Debt Stock Levels

Debt creation has continued unabated over the last decade. The global debt stock has not only reached new highs in absolute terms, but also when we consider the global debt-to-GDP ratio. The two elephants in the room are China and the U.S., two countries engaged in a long-term trade war in our view. Debt creation has been primarily generated through the corporate and government sectors. We observe a plethora of highly levered companies with the inability to generate positive cash flow to trade at unrealistic valuation levels. The divergence between company fundamentals and the stock price is striking, as if cheap financing is warranted over foreseeable future.

- US & China Trade War Saga

The escalation process that began in early 2018 continues to have negative consequences, not only for the world's largest two economies, but globally. The slump in global manufacturing activity illustrates the impact of a lasting trade war situation. A long-term agreement between the both parties currently in place seems unlikely. If the U.S. trade deficit with China, which started to progressively build since the 80’s doesn’t correct, the trade war could remain a dominant theme in the coming years.

- Weakening Global Growth

The curbing investment cycle combined with the contraction in manufacturing activity, brings some developing countries to the brink of an economic recession. Several central bankers are calling for fiscal stimulus as a transition to the waning monetary policy impact. However, given the already large debt stock, not all countries have the same level of flexibility.

- Risk Concentration

With investors forced to chase yields, global portfolios will naturally start to exhibit higher correlations. We view this setup as presenting a significant source of opportunities for active managers. Currently, equity markets offer strong alpha opportunities at various levels: equity factor, sector and single name. Consequently, portfolio diversification is of even greater importance today.

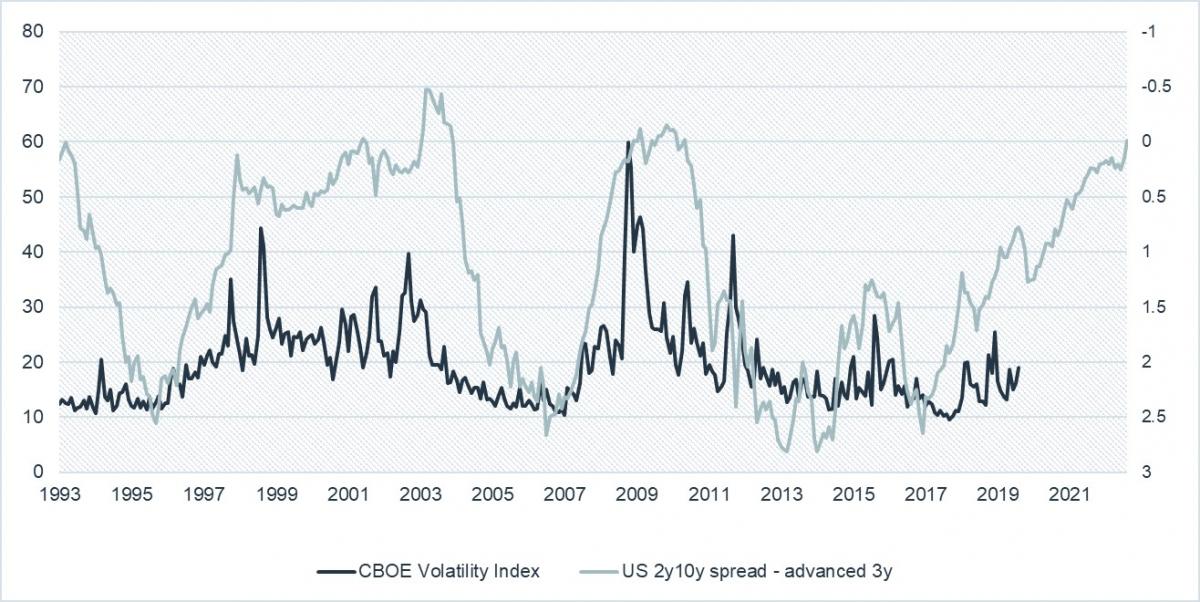

- The Predictive Powers of Bond Yield Curves

Additionally, the shape of the yield curve in developed countries remains an effective predictor of economic growth and future volatility. The below chart illustrates the long-term behavior of the U.S. interest rates curve (2y & 10y) and the equity market volatility, there appears to be a clear relationship between the two measures, advocating for the fact that a volatility regime change is likely to happen in the coming quarters.

2Y10Y US TREASURY SPREAD (ADVANCED 3Y) VS VIX INDEX

Source: Bloomberg, RAM Active Investments, as of 31.08.2019

In such a context, we are convinced that diversification and uncorrelated investment solutions with proven track records bear higher importance in a portfolio context.

RAM Long/Short European Equities – a lowly correlated solution with robust fundamentals

Our European Long/Short Equities Strategy is well positioned to benefit from the inefficiencies we observe in this market:

- Asymmetry of fundamentals between long and short positions: on average long positions exhibit much stronger fundamentals than short positions. For instance, the free cash-flow yield of the long book is 8.3% vs -3.0% for the short book.

Source: Bloomberg, RAM Active Investments, as of 31.08.2019

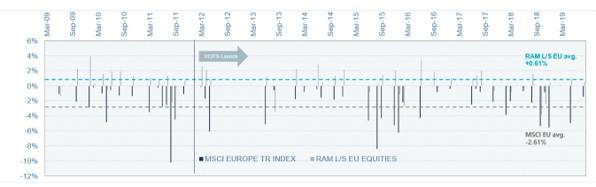

- Uncorrelated behavior in down markets: during down months for the MSCI Europe Index (-2.61% average monthly loss since March 2009), The RAM Long/Short European Equities Strategy was able to generate an average monthly gain of +0.61%.

RAM LONG /SHORT EUROPEAN EQUITIES PERFORMANCE DURING DOWN MONTHS FOR MSCI EUROPE TR INDEX

Source: Bloomberg, RAM Active Investments, as of 31.08.2019

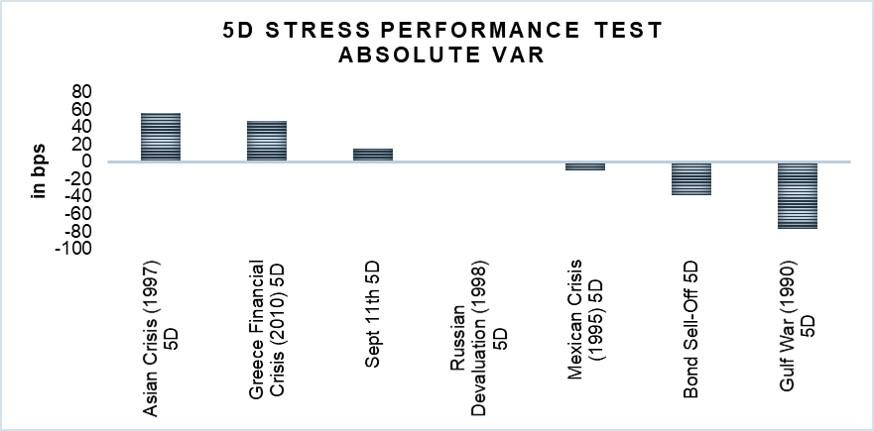

- Resilient behavior during market stress periods: stress testing of the RAM Long/Short European Equities Strategy shows that if one of the historical stress events were to occur, the Fund would be resilient:

Source: RiskMetrics, RAM Active Investments, as of 31.10.2019

- Stabilisation and beginning to capture inefficiencies: during the last seven months, the Strategy has been relatively stable despite the large moves within European equity markets, supporting the fact that dispersion has reached extreme levels in Europe and we are seeing the start of a reversal.

Bloomberg, RAM Active Investments, as of 30.10.2019

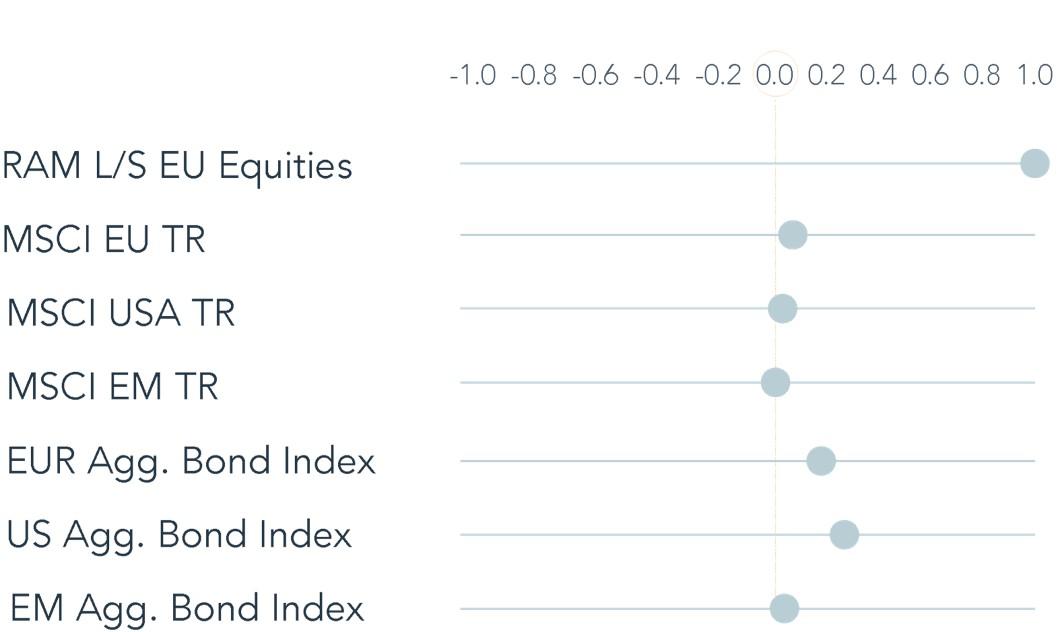

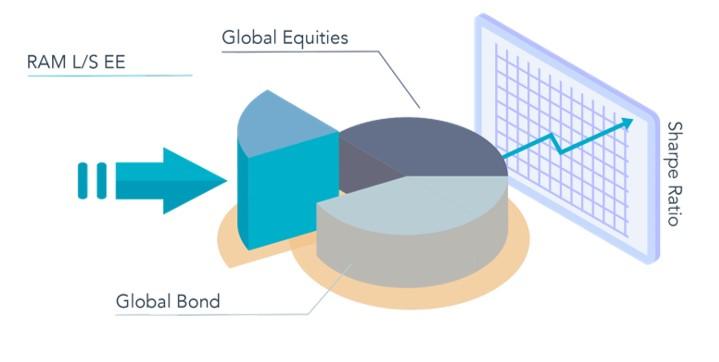

- A true portfolio diversifier: the portfolio has a low correlation to equity and bond indices; a marginal allocation to the RAM Long/Short European Equities Strategy, increases the Sharpe ratio of a portfolio composed of global equities and bonds.

Correlation of RAM L/S Equities vs Indices

RAM L/S European Equities added to a portfolio of Global Equities and Bonds

Finally, it is important to remind that the Strategy focuses on:

- Liquidity

- Diversification

- All cap exposure

- Efficient and rapid integration of new information

Direct access per fund to our latest Fund Manager's Comments:

Legal Disclaimer

This document has been drawn up for information purposes only. It is neither an offer nor an invitation to buy or sell the investment products mentioned herein and may not be interpreted as an investment advisory service. It is not intended to be distributed, published or used in a jurisdiction where such distribution, publication or use is prohibited, and is not intended for any person or entity to whom or to which it would be illegal to address such a document. In particular, the products mentioned herein are not offered for sale in the United States or its territories and possessions, nor to any US person (citizens or residents of the United States of America). The opinions expressed herein do not take into account each customer’s individual situation, objectives or needs. Customers should form their own opinion about any security or financial instrument mentioned in this document. Prior to any transaction, customers should check whether it is suited to their personal situation and analyse the specific risks incurred, especially financial, legal and tax risks, and consult professional advisers if necessary. The information and analyses contained in this document are based on sources deemed to be reliable. However, RAM AI Group cannot guarantee that said information and analyses are up-to-date, accurate or exhaustive, and accepts no liability for any loss or damage that may result from their use. All information and assessments are subject to change without notice. Investors are advised to base their decision whether or not to invest in fund units on the most recent reports and prospectuses. These contain further information on the products concerned. The value of units and income thereon may rise or fall and is in no way guaranteed. The price of the financial products mentioned in this document may fluctuate and drop both suddenly and sharply, and it is even possible that all money invested may be lost. If requested, RAM AI Group will provide customers with more detailed information on the risks attached to specific investments. Exchange rate variations may also cause the value of an investment to rise or fall. Whether real or simulated, past performance is not necessarily a reliable guide to future performance. The prospectus, key investor information document, articles of association and financial reports are available free of charge from the SICAVs’ and management company’s head offices, its representative and distributor in Switzerland, RAM Active Investments S.A., Geneva, and the funds’ representative in the country in which the funds are registered. This marketing document has not been approved by any financial Authority, it is confidential and its total or partial reproduction and distribution are prohibited. Issued in Switzerland by RAM Active Investments S.A. which is authorised and regulated in Switzerland by the Swiss Financial Market Supervisory Authority (FINMA). Issued in the European Union and the EEA by the authorised and regulated Management Company, Mediobanca Management Company SA, 2 Boulevard de la Foire 1528 Luxembourg, Grand Duchy of Luxembourg. The source of the above-mentioned information (except if stated otherwise) is RAM Active Investments SA and the date of reference is the date of this document, end of the previous month.