Articles & Interviews

8 September 2025

Enhancing Portfolios Beyond Traditional Exposures

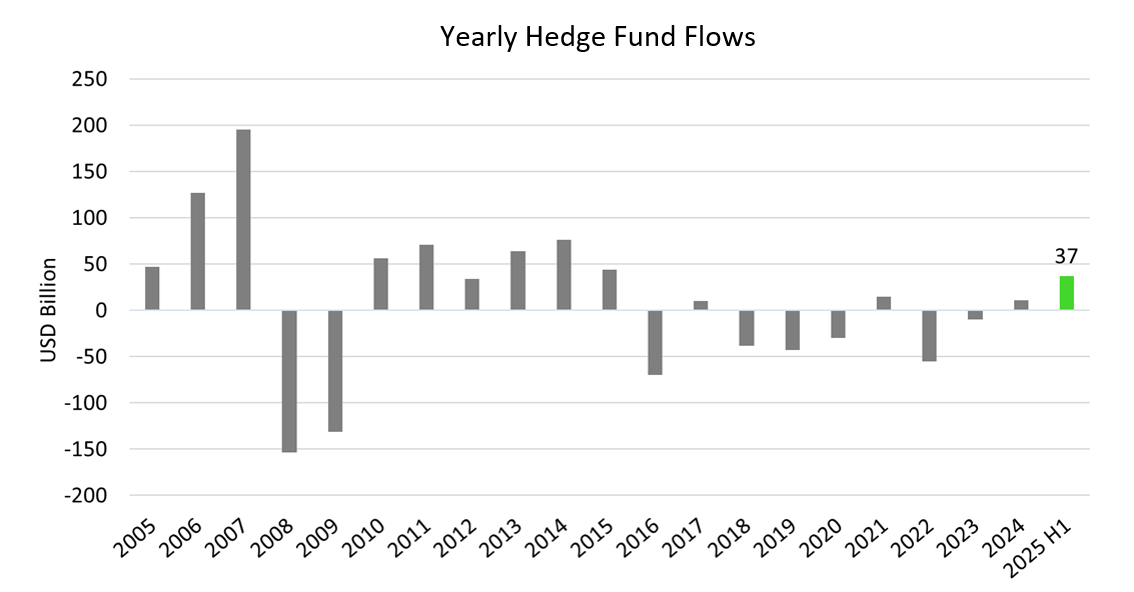

In an environment where risk asset valuations remain stretched and equity/bond correlations persist, hedge fund flows provide a useful gauge of investors’ demand for diversification. The chart below illustrates yearly hedge fund flows, showing that 2025 is shaping up to be the strongest year for inflows in more than a decade. In the first half alone, the industry attracted over USD 37 billion in new capital, underscoring a clear investor preference for strategies that balance risk, enhance resilience, and deliver uncorrelated returns.

Source: Bloomberg, HFR, as of 30.06.2025

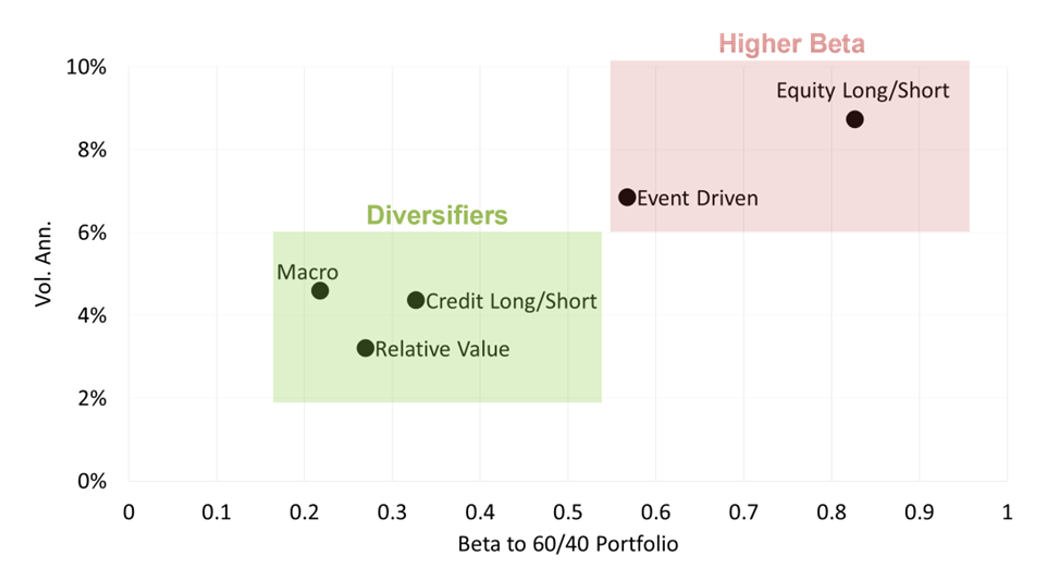

Hedge funds, as an asset class, can enhance portfolio resilience. However, understanding strategy cyclicality and sensitivity to market direction is critical. For investors seeking traditional portfolio diversifiers, an effective addition should provide:

• Consistent risk management

• Superior risk-adjusted returns

• Low dependence on market direction

In this context, the distinction between ‘Diversifiers’ and ‘High Beta’ hedge funds is essential to strengthening portfolio robustness and supporting long-term outcomes. The chart below illustrates the beta of broad hedge fund categories to a 60/40 global portfolio alongside their volatility. Relative Value, Macro, and Credit Long/Short strategies appear to offer the diversification benefits needed at a time when risk-adjusted returns come back into consideration.

Source: Bloomberg, RAM AI, as of 30.06.2025

Note: Statistics based on monthly performance figures in USD over 10 years

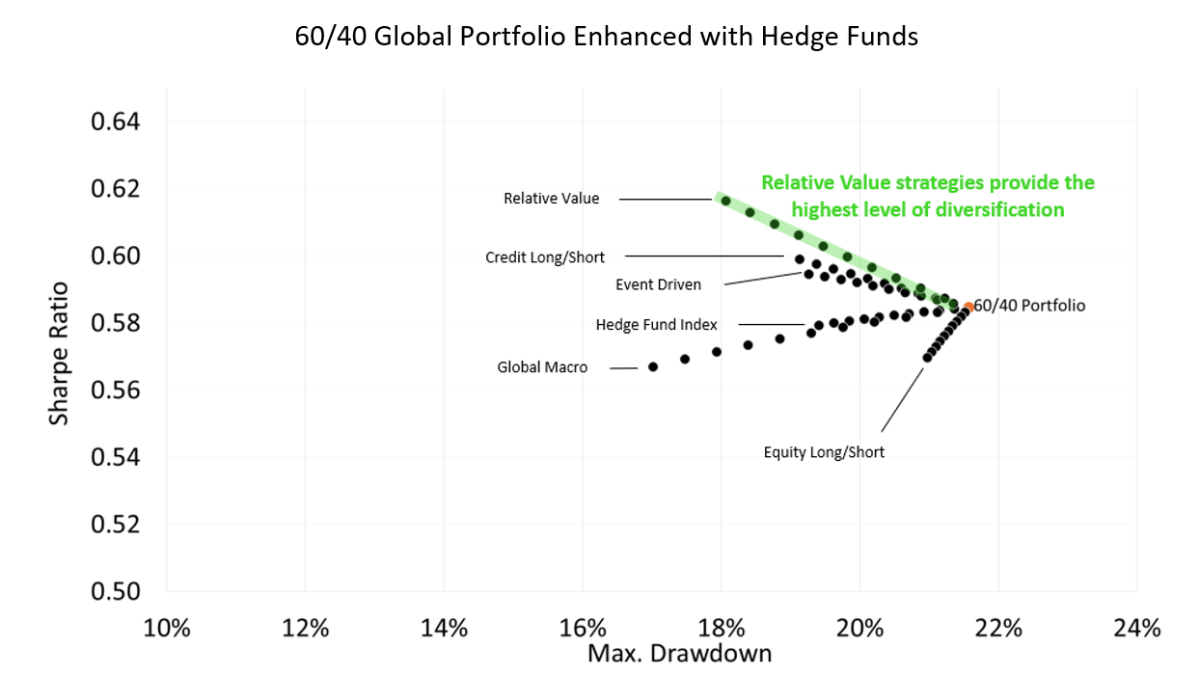

The simple exercise of adding hedge fund strategies to a 60/40 global portfolio – in 2% increments from 2% to 20% – highlights the advantages of Relative Value strategies over the past 10 years, delivering the greatest reduction in maximum drawdown and the strongest enhancement in Sharpe ratio.

Source: Bloomberg, RAM AI, as of 30.06.2025

Note: Statistics based on monthly performance figures in USD over 10 years

Strategies within the Relative Value category include Equity Market Neutral, Fixed Income Arbitrage, Convertible Bond Arbitrage, Statistical Arbitrage, Volatility Arbitrage, and Multi-Strategy. It is important to note that the ‘Higher Beta’ category also contains valuable hedge funds within Equity Long/Short and Event Driven strategies that can serve as portfolio diversifiers. The current analysis is solely based on broad hedge fund categories, with the aim of guiding the search for strategies that enhance portfolio diversification.

Finally, when investing in hedge funds, beyond the core pillars of investment, risk, and operational due diligence, we believe the notion of “adequacy” should also take center stage. This encompasses considerations such as asset/liability liquidity, fee structures, and alignment of interests. While some of these elements are sometimes overlooked in exchange for privileged access, history tells us that not all industry trends ultimately serve the best interests of every party involved.

by Hasan Aslan

Allocator & Senior Portfolio Manager